Bad Loans given for the wrong reasons

If you are old enough to remember the Crash of 2008 you may or may not know that what caused it was a law requiring banks to make home loans (mortgages) to people with a very high risk of not being able to pay them back. These rules were supposed to help people buy houses who normally wouldn’t qualify. But they couldn’t afford the payments in the end.

“By cutting out the middleman, we’ll save American taxpayers $68 billion in the coming years,” the president said. “That’s real money — real savings that we’ll reinvest to help improve the quality of higher education and make it more affordable.”

President Obama https://abcnews.go.com/WN/Politics/health-care-obama-signs-student-loan-overhaul-legislation/story?id=10239569

“The result of the government’s expansion into the subprime mortgage market was that by the time of the financial crisis, more than half of all mortgages in the United States were subprime or otherwise low-quality mortgages, and the various federal government agencies were directly backing 76 percent of them.” https://fee.org/articles/how-the-federal-government-created-the-subprime-mortgage-crisis/

When banks loan money they consider the ability of the borrower to pay it back. There is a wealth of data available that predicts who will pay it back on time, late, or never. You have to have some kind of income source and they check your credit history to see if you paid back other loans.

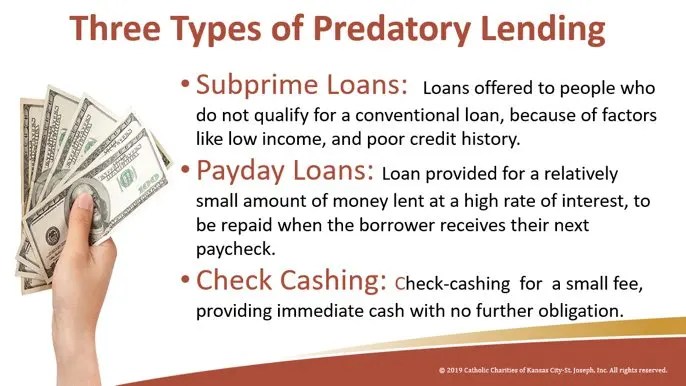

People with bad credit history will pay higher interest rates because the bank is presuming there is a higher risk they won’t get their money back. People with really bad credit may have to resort to shady lenders such as payday loans, title loans, pawn shops, and private loan companies and pay very high interest. They may have to sign over their paychecks or the title to their vehicle.

Obama’s Student Loan Legislation

The student loan program does the same thing. In 2010 President Obama decided that the government would now take on the full risk for student loans and become the actual lender through the US Treasury instead of letting banks make the loans. By doing so he propped up the US economy with risky loans and secured his second term in office.

Now that the government is in the student loan business, it is giving loans to people with a high risk of defaulting: people with no jobs, no prospects, and no family history of financial responsibility.

The reality is that in many cases these loans are PREDATORY LENDING. The schools that have the highest default rate are for-profit schools, not public colleges. These schools promise that you will graduate with a skill that will enable you to be more competitive in the job market. Unfortunately, what actually happened is that many of these jobs have very low starting pay and with the constantly increasing cost of living, many borrowers do not make enough money to pay bills and their student loan payments. That is IF they find a job at all.

By requiring people to pay for training that could easily be taught ON THE JOB, the businesses are able to ration low paying jobs and save themselves money. In our current high-tech economy there are not as many entry level jobs available that pay more than minimum wage.

It’s unfortunate but true that many lower-income borrowers do not understand that they are signing their life away for that student loan for a job that might not even exist. School counselors are not helping students make good educational choice, but even more, some borrowers are just not able to do some of the jobs they are going to school for. They get the debt, but they can’t pass the classes or succeed at the job if they get one. They end up with a default and still in the same low income boat. Obviously there are success stories but there are more defaults by people who started out at the bottom.

While prior work has raised alarm bells about the crisis for African-American borrowers (Miller, 2017), the new data should ring the alarm even louder. As shown in Table 2, nearly 38 percent of all black first-time college entrants in 2004 had defaulted within 12 years, a rate more than three times higher than their white counterparts, and 13 percentage points higher than black students entering just eight years prior. Focusing on borrowers only and projecting default rates out through year 20 (as shown in Figure 3) suggests that 70 percent of black borrowers may ultimately experience default.

https://www.brookings.edu/research/the-looming-student-loan-default-crisis-is-worse-than-we-thought/

Not many people were aware that Obama had pulled a student loan switcheroo and hid it in the final health care reconciliation bill that no Republicans voted for. At that time the economy was so bad and most Conservatives were so mad about Obamacare that they didn’t notice the student loan changes. https://abcnews.go.com/WN/Politics/health-care-obama-signs-student-loan-overhaul-legislation/story?id=10239569

Success requires more than a degree

Going to college has been held up as the cure for poverty. But like all social problems, such as homelessness, crime, and drugs, there is no quick and easy way to ensure everyone is successful in life. Going to college is a waste of money for some people. “Going to college and getting a degree” doesn’t magically make someone smart or qualified. Growing up in poverty usually has lasting effects on learning abilities and attitudes.

It takes a lot of motivation to study and graduate from college, which is why employers respect that degree. But the list of desired qualifications in a job description goes beyond technical skills . Employers are looking for people with personal and character attributes such as leadership ability, teamwork, punctuality, self-motivation, ability to work without supervision, positive attitude, ability to work in a fast-paced environment, etc..

I have been reading job descriptions lately and companies expect a lot for $12 an hour, including job experience. In fact, job experience is mentioned more often in low-paying positions than you might think. This means that even the lowest paid jobs are hard to get for people just entering the job market. And having a degree or certificate with no experience still puts you at the bottom of the list. Therefore, students should work or volunteer within their field of study while still in school to build experience.

Businesses also prefer to hire someone with good references and especially references from someone they trust. In other words, networking and connections are very important in the job search. And many people who are first generation college graduates lack this benefit because their parents are either unemployed or work in jobs with people that can’t help them. This means that schools should be helping students understand the importance of developing some connections in their field of choice that can vouch for them when they start looking for a job.

Besides networking and connections, if college is going to have a lasting impact on their lives and break the cycle of family poverty, some students will need to be taught study skills, stress management, basic life skills and also have expectations and consequences for their choices during college. This could be part of the requirements for continuing to receive financial aid and living expenses. The students who are motivated to do well would be willing to participate.

In addition, some students are required to take (and pay for) remedial classes to learn how to read at college level and do college math because many graduate from public high school with a subpar education. Students are often negative about these classes and end up dropping out.

Moreover, the problem is worse for low-income students and students of color, whose rates of remedial education enrollment are higher than for their white and higher income peers. According to a recent study, 56 percent of African American students and 45 percent of Latino students enroll in remedial courses nationwide, compared with 35 percent of white students.

https://www.americanprogress.org/article/remedial-education/

Summary

The student loan program was intended to enable more people to go to college and have a chance to succeed in a world where good jobs that don’t require higher education are scarce. They also provide billions of dollars to for-profit, private, and public schools which is part of the GDP. Thus, student loans are a help fuel the US economy.

Obama passed legislation that completely changed how the student loan program works. It was included in a health care act reconciliation bill that no Republicans voted for. The changes made it so that the US Treasury now acts as the bank for student loans.

The student loan program is similar in effects to the legislation that forced banks to give loans to unqualified borrowers in that it gives loans to students that are unlikely to pay back the loans. The housing loans led to the worst recession since the Great Depression in 2008 when millions of these bad loans defaulted. Now the Biden administration wants to forgive student loans.

Predatory loans are loans with high interest rates and fees that are given to people with bad credit. Student loans are predatory when they are given to students who don’t understand the repayment terms, have high or compounded interest, who aren’t receiving a quality educations or have low odds of getting a job after school. Data is available that shows which students are more likely to default.

Higher education must be combined with personal habits, character traits, connections, and motivation to create success. Many students from low income high schools need remedial education which is a predictor of dropping out of classes. Public schools must be held accountable for graduating illiterate students.

Questions

Are all the costs associated with the student loan program worth it if it enables a portion of low income borrowers to get a better start in life? While having a degree has been correlated in general with higher earnings, the question remains: does going to college actually help break the cycle of poverty? Or is the student loan program simply a money factory for colleges? Is our entire economy a house of cards built on fiat money? What will happen when the public finds out?

Thank you for a great article explaining in detail about the housing crisis and student loans. Fannie and Freddie macs made subprime mortgages. Banks pooled the risk with more secure loans and created mortgage-backed securities. They were sold to the public and eventually tanked when borrowers couldn’t make the balloon payments on their subprime loans. Also, today I read an article that explains the fine print on today’s student loan forgiveness.

“Biden would roll back borrowers’ maximum monthly payment on undergrad loans to just 5% of “discretionary” income — and cut the amount of earnings considered “discretionary.” Then he’d wipe out all remaining debt after just 10 years for many borrowers.” — NY Post

Right. It’s a bailout .

👍🏼

Not everyone SHOULD go to college. Case in point, my wife was the first to begin an online class at her University. She would screen students with a questionnaire to make sure they were self-disciplined and informed enough to take an online class.

When the college administrators got wind of her process (several YEARs after she had started), they assumed, “Well, it’s online; anyone can do that, and the teacher doesn’t even have to work.” 🙄 Doh!

So now her class has to be open to all who want to sign up, and EVERY semester she will get two or three emails from students, “The handbook does not say what room our class meets in.”

Besides the poor grammar (“…in what room our class meets.”), it is ONLINE! 😂😂

I agree and yet it’s really hard to tell people, you aren’t cut out for college.

Yes, their expectations were raised by the government and the hard sell ‘you can be anything you want to be if you go to college.’

Hello.

Many thanks for your post if I may answer your questions at the end of your post.

“Are all the costs associated with the student loan program worth it if it enables a portion of low income borrowers to get a better start in life?”

No, governments never spend taxpayers money well nowadays, and it doesn’t encourage responible attitudes to using money wisely.

“While having a degree has been correlated in general with higher earnings, the question remains: does going to college actually help break the cycle of poverty?”

No, many people would do much better on apprenticeships as used to be practiced. This is best done by smaller businesses and if they weren’t taxed so highly in some quarters could take on someone.

“Or is the student loan program simply a money factory for colleges?”

Yes, and for the banks who becoming too large are considered too large not to bail out in a crisis, at least in the UK that is.

“Is our entire economy a house of cards built on fiat money?”

Yes, when the big bad wolf of inflation comes along he will huff and he’ll puff and everything falls down.

“What will happen when the public finds out?”

A good question. Will they be in so much debt it’s too late? Money is artificial anyway. A useful tool up to a point but an awful master. And you can’t eat it!