After spending a few hours researching, these are my conclusions and notes. I decided to leave it all in there for those who might want to read it. I know it’s a lot. Read or listen, your choice! ( I had difficulty getting the embed link to work. Let me know if you have trouble. ) Here is another option. https://podcasters.spotify.com/pod/show/blueskiesandgreenpastures/episodes/Will-2023-be-known-as-the-Year-of-Uncertainty–Current-Events-Roundup-March-2023-S3E11-e21cg3u/a-a57pj3

I know that I am not alone in feeling like the world is a little bit out of control at the moment. Yet I am confident that God is still in charge. Along with the bad news, I am encouraged by the many stories I am reading of people coming to Christ or drawing closer to God. It certainly does feel like we are seeing signs of the last days. I think it’s important to look for the positive changes, focus on loving our own families and friends, and continue to pray and study the Word. This is how we do not fall into the trap of fear or let our hearts grow cold even while the world is getting more chaotic. Our hope is in the Lord who does not change. He is with us always. We can trust Him.

Every day some new financial announcement, tech news about AI dangers, or terrible tragedy such as the Turkey earthquakes, Mississippi tornado or the Tennessee mass murder catches my attention, but because I like to research a topic before I write, I have not been able to keep up with these rapid-fire current events. I’ve done a lot of reading, watched a lot of videos, and listened to countless podcasts on these subjects.

Side note: Some people might wonder why I study this stuff. I like it! Finances and business are actually one of my interests.

Changes in the Economy

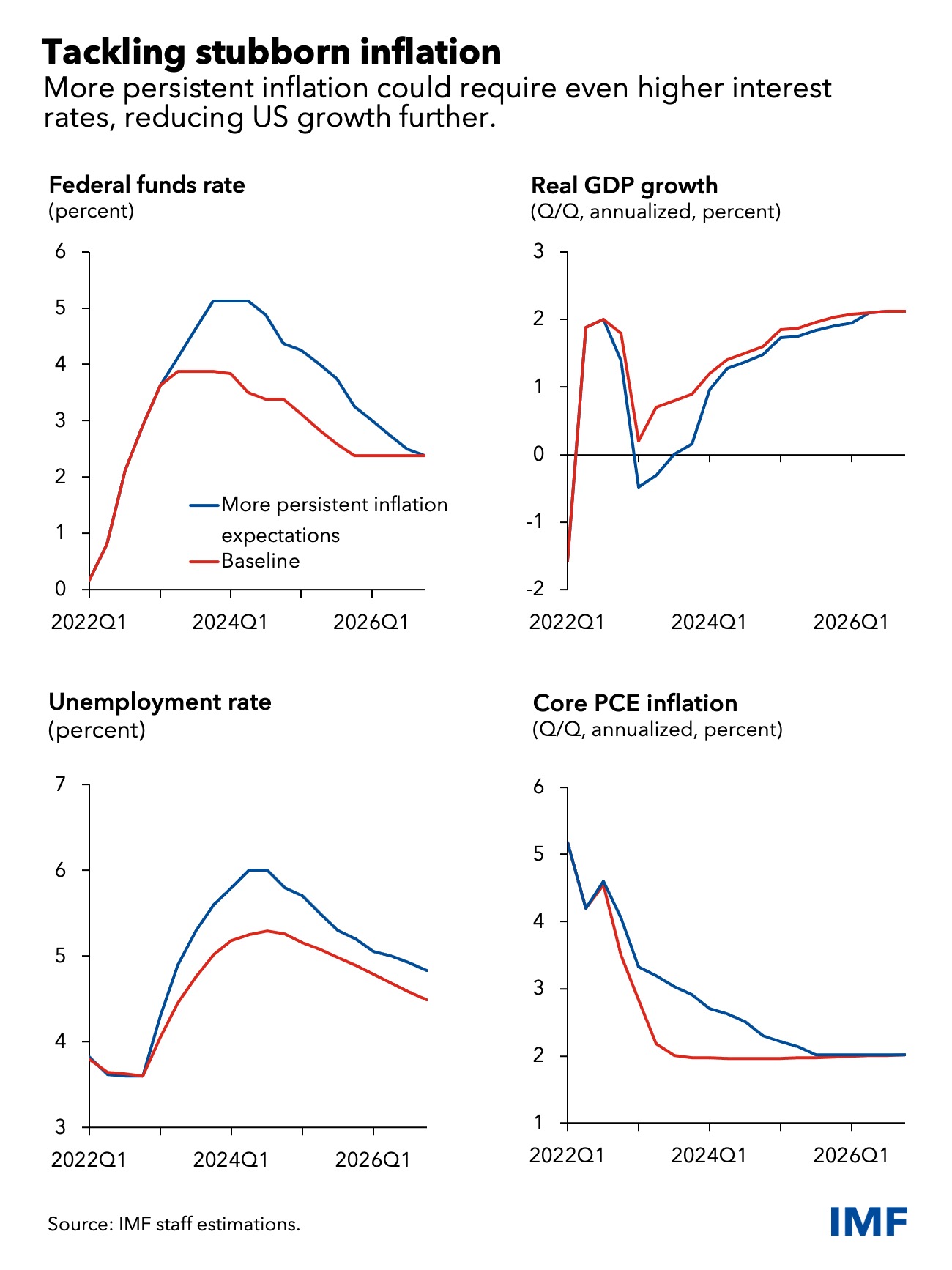

Concern over the stability of the US economy is rising due to persistently high inflation, investment bank failures, and tech layoffs. People in all income brackets have been affected. The working poor suffer the most from inflation, but the investor class has also lost billions, the tech industry is on shaky ground, and supply chain issues are affecting everyone. All of these things existed well before the Covid pandemic, however they were worsened by the Covid stimulus, forced business closures, and travel restrictions between countries.

The increase in spending on consumer goods thanks to people staying home and being given stimulus checks and reduced spending on services during the pandemic have not returned to normal levels, nor have all people returned to their jobs. Some have decided to retire and others have been living off of previously implemented Covid assistance. But with the recent end of the supplemental Food Stamp funding, that might change soon. The Federal Reserve has continued to attempt to lower inflation by raising rates which has slowed the overpriced housing market by 40% since a year ago as well as led to tightened lending and reduced demand for loans.

Most people agree that we are in a recession. However there are some signs that the Feds efforts are working to balance out the economy. Not everyone is happy though. Bonds bought when the rates were low are now worth less money than bonds bought at the higher rates. This has caused banks to lose money. The stock market has also slowed down. Also new and adjustable home mortgage rates and adjustable credit card rates will be higher.

The following is a summary of past and present factors that have contributed to the instability of our economy. While these are concrete examples of policy decisions, personal actions and government reactions, I think the important takeaway is this: speculation, rather than producing real goods and benefits to society plays too big of a role in the US economy. And the reason for speculation is human nature.

People want to get rich quick. They may be poor and desperate or they may be rich and greedy, but they invest it in risky things or they invest it without enough knowledge of the risks. That includes our own government and those who are supposed to be regulating the financial markets to protect those of us who do not take these financial risks. This willingness to risk other people’s money is the real cause of the current economic situation. This is not simply buying stocks in proven companies.

Some types of investment behavior are gambling, but not all. For example, earning interest is not gambling. But that is not where the real money is. If you want to win big, you have to take risks. Some gamble on technology or pharmaceuticals that might not ever produce profits. Some gamble on the failure of certain ventures. Others attempt to create those failures by putting out bad news about companies. At this time there are even people hoping that we will see the value of the dollar collapse so they can usher in a bank-free world and cash in on their crypto investment, although that is not a logical outcome. The money comes from getting in and out at the right time. The gambler becomes obsessed because he has a lot to lose or gain. It can become a real addiction.

Human nature creates a dilemma for those of us who want both freedom and protection from the mistakes of others. At the heart of this debate is the question of whether people are capable of handling the responsibility that comes with freedom. Some argue that individuals are best equipped to make decisions about their own lives and that the government should not interfere unless absolutely necessary. Others contend that people are prone to irrationality, biases, and self-interest, and that government intervention is needed to protect the public good.

I think we can look at the past and present and see that while some have benefited greatly from the lack of regulation, many more have been hurt. It is time to admit that unless we better educate people on potential losses and provide some type of barriers to entry to investing, as well as much stronger and less political monitoring of the market, it is just too dangerous to allow Wall Street so much freedom.

A second, equally important, conclusion from my research is that Americans in general have very little knowledge how money works, how banks work, or what the monetary system is. The average worker who puts their money into a 401k never questions where the money goes or if it is safe.

According to https://www.cbsnews.com/news/401k-millionaires-fidelity-stock-market-hits-retirement-savings/ “The number of 401(k) accounts with at least $1 million in retirement savings fell 32% last year, to 299,000, from 442,000 in 2021, according to new data from Fidelity Investments. The shrinking number of 401(k) millionaires comes after the S&P 500 tumbled 19.4% last year and entered the longest bear market since the 2008 financial crisis. The downturn has marked a sharp departure from the prior decade, when a bull market buoyed investment portfolios and appeared to place a comfortable retirement within reach for many workers.”

And people in general have very short memories. 2008 was not that long ago, but many of today’s younger workers do not remember the bad times. They do not understand that markets have been propped up with zero or almost zero interest rates. We have put way too much trust in the Federal Reserve, the Treasury Department, and the SEC to know what to do and to do the right thing. I blame our education system and government for allowing the public to become so dependent and uninformed.

A third conclusion is that the US may be at the end of it’s 100 year run of being the world’s top economy. Oil, petrodollars, innovation and our military made us rich and powerful. We were able to import cheap goods from developing nations and sell our dollars and goods to other countries. But now, things are changing. We will have to adapt to the new geopolitical and economic landscape if we are to remain strong and free. https://www.ey.com/en_gl/geostrategy/future-of-globalization

Notes and Explanations

The 2008 Financial crisis

The 2008 financial crisis was caused by a complex combination of factors related to inadequate regulation and oversight of financial institutions, and a lack of transparency in the financial system. In short, no one was paying attention to what was happening on Wall Street.

Here are some examples of the groups or entities that could be associated with each of the five categories of responsibility for the 2008 financial crisis:

- Financial institutions: Examples of financial institutions that engaged in risky behavior leading up to the crisis include Lehman Brothers, Bear Stearns, and AIG.

- Rating agencies: Examples of rating agencies that provided inflated ratings to risky financial instruments include Moody’s, Standard & Poor’s, and Fitch Ratings.

- Regulators: Examples of regulatory agencies that failed to adequately oversee and regulate the financial industry include the Federal Reserve, the Securities and Exchange Commission (SEC), and the Office of the Comptroller of the Currency (OCC).

- Politicians: Examples of politicians who promoted policies that contributed to the crisis include President George W. Bush, who pushed for increased access to home ownership, and Senator Chris Dodd and Congressman Barney Frank, who co-authored the Dodd-Frank Act in response to the crisis.

- Investors: Examples of investors who engaged in risky investments include many hedge funds and other institutional investors, as well as individual investors who purchased risky financial products without fully understanding the risks involved.

One key figure in the push for increased lending by Fannie and Freddie was Congressman Barney Frank, who was the Chairman of the House Financial Services Committee from 2007 to 2011. Frank was a strong supporter of Fannie and Freddie, and he advocated for policies that would increase their role in the mortgage market and expand access to home ownership.

Other key figures in the push to expand Fannie and Freddie’s purchases of mortgages included the leaders of the two entities themselves, as well as government officials such as Treasury Secretary Henry Paulson and Federal Reserve Chairman Alan Greenspan. These individuals believed that Fannie and Freddie played an important role in promoting home ownership and providing liquidity to the mortgage market, and they argued that expanding their purchases of mortgages would help to stabilize the housing market and promote economic growth.

Henry Paulson was the U.S. Treasury Secretary from 2006 to 2009, and he played a key role in responding to the 2008 financial crisis. Prior to his appointment as Treasury Secretary, Paulson was the CEO of Goldman Sachs, one of the largest investment banks on Wall Street.

In his role as Treasury Secretary, Paulson was involved in efforts to stabilize the housing market and prevent the collapse of major financial institutions. He advocated for the government’s bailout of Fannie Mae and Freddie Mac in 2008, as well as the Troubled Asset Relief Program (TARP), which provided capital injections to banks and other financial institutions that were struggling in the wake of the crisis.

However, some critics argue that Paulson’s actions as Treasury Secretary contributed to the crisis by failing to adequately regulate the financial industry and allowing risky lending practices to go unchecked. For example, as CEO of Goldman Sachs, Paulson was involved in the creation and sale of complex financial instruments such as mortgage-backed securities, which played a key role in the housing bubble and subsequent collapse.

Alan Greenspan was the Chairman of the Federal Reserve from 1987 to 2006, and he is widely credited with playing a key role in shaping the U.S. economy during this time period. During his tenure, Greenspan was known for his support of free markets and deregulation, and he was a strong advocate for policies that encouraged home ownership and economic growth.

However, some critics argue that Greenspan’s policies contributed to the housing bubble and subsequent financial crisis by failing to adequately regulate the financial industry and promote responsible lending practices. For example, Greenspan supported the expansion of Fannie Mae and Freddie Mac’s purchases of mortgages, including subprime mortgages, and he opposed efforts to regulate the derivatives market, which played a key role in the financial crisis. After the crisis, Greenspan acknowledged that his belief in free markets and deregulation may have been misplaced, and he expressed regret for some of his policies and decisions during his tenure at the Fed.

In the years leading up to the crisis, many financial institutions had taken on large amounts of debt and had made risky investments in the housing market, which was experiencing a bubble. When the housing market began to decline and homeowners started defaulting on their mortgages, the value of these investments plummeted, leading to widespread losses and a credit crunch.

Additionally, the interconnectedness of financial institutions meant that the failure of one institution could have a ripple effect throughout the entire financial system, leading to a systemic risk that threatened the stability of the global economy.

Both Democrats and Republicans were involved in the push to expand Fannie Mae and Freddie Mac’s purchases of mortgages, including subprime mortgages, and both parties bear some responsibility for the policy decisions that contributed to the 2008 financial crisis.

For example, the Community Reinvestment Act (CRA), which required banks to make loans to underserved communities, was passed in 1977 during the Carter administration, but it was expanded and strengthened during the Clinton administration in the 1990s. This expansion of the CRA, along with other policies aimed at promoting home ownership, contributed to the housing bubble and subsequent collapse.

In summary, the 2008 financial crisis was the result of a combination of factors, including a housing bubble, risky financial practices, inadequate regulation, and systemic risks in the financial system.

Bitcoin

Bitcoin was created directly after the 2008 financial crisis in 2009 by an anonymous person or group known only as “Satoshi Nakamoto,” and it has since become one of the most popular cryptocurrencies in the world.

Bitcoin was designed as a decentralized digital currency that could be exchanged between users without the need for intermediaries such as banks or payment processors. In practice, bitcoin is more of an asset or commodity, although a few businesses do now accept it as a currency.

Since the introduction of Bitcoin, many other cryptocurrencies have been developed, each with their own unique features and use cases. Some of the most popular cryptocurrencies include Ethereum, Litecoin, and Ripple. These assets are collectively referred to as “altcoins” or “alternative coins.”

A stablecoin is a special type of cryptocurrency that is designed to maintain a stable value relative to a particular asset or basket of assets, such as the US dollar or a commodity like gold. This is in contrast to other cryptocurrencies like Bitcoin, whose value is determined by supply and demand in the market and can be highly volatile.

The basic idea behind Bitcoin is that it provides a decentralized, peer-to-peer network for users to send and receive payments without the need for intermediaries like banks or other financial institutions. This is made possible through the use of a blockchain, which is essentially a digital ledger that records all Bitcoin transactions.

The blockchain works by using complex algorithms to verify and confirm transactions, which are then added to the blockchain as a new “block.” Each block contains a unique code or “hash” that links it to the previous block in the chain, creating a secure and tamper-proof record of all Bitcoin transactions.

One of the key benefits of Bitcoin is that it provides users with a high degree of anonymity and privacy when making transactions. Because the blockchain is decentralized and transactions are not linked to any particular individual or organization, it can be difficult to trace Bitcoin transactions back to their source.

However, this anonymity can also be a double-edged sword, as it makes Bitcoin transactions attractive to criminals and other illicit actors. For example, Bitcoin has been used to fund illegal activities such as drug trafficking, money laundering, and terrorism.

Another potential danger of Bitcoin is its extreme volatility. Bitcoin prices have fluctuated wildly over the years, with dramatic peaks and valleys that can result in huge gains or losses for investors. This volatility can make Bitcoin a risky investment, as it is difficult to predict how its value will change over time.

PONZI

Ponzi scheme is a fraudulent investment scheme where returns are paid to earlier investors using the capital of new investors, rather than from profits generated by the investment. The scheme relies on the continuous recruitment of new investors to pay off earlier investors, rather than on any legitimate business activity.

Some people believe that Bitcoin is a Ponzi scheme because they see similarities between the two. They argue that early adopters of Bitcoin made significant profits, and the value of Bitcoin has increased over time, making it seem like a good investment opportunity. However, they claim that the only reason Bitcoin has value is that people believe it has value, rather than any underlying asset or revenue-generating activity.

Furthermore, they argue that Bitcoin’s decentralized nature and lack of regulation make it easy for scammers to promote it as a get-rich-quick scheme, attracting unsuspecting investors who are lured by the promise of quick and easy profits. As more people invest, the value of Bitcoin increases, and early adopters cash out, leaving later investors holding the bag.

Additionally, Bitcoin is still a relatively new technology, and there are many unanswered questions about its long-term viability and sustainability. For example, the massive amount of energy required to mine Bitcoin has raised concerns about its environmental impact, while its reliance on complex algorithms and cryptography could potentially make it vulnerable to hacking or other forms of cyber attack.

Despite these potential risks, Bitcoin remains a popular and widely used cryptocurrency, and it has attracted a passionate community of users and supporters. Many people see Bitcoin as a way to decentralize and democratize the global financial system, while others view it as a speculative investment or a hedge against inflation and other economic uncertainties.

A significant selloff in Bitcoin could potentially have ripple effects on the broader economy, although the exact extent of the impact would depend on a variety of factors, including the magnitude and duration of the selloff, as well as the level of exposure of different market participants to Bitcoin.

Here are some potential impacts that could occur:

- Wealth effects: A selloff in Bitcoin could result in significant losses for investors who have exposure to the cryptocurrency, potentially reducing their overall wealth and leading to a decrease in consumer spending.

- Financial stability: If the selloff is large enough, it could potentially cause distress in the financial system, particularly for firms that have significant exposure to Bitcoin. For example, if banks or other financial institutions have made loans to firms that are heavily invested in Bitcoin, a selloff could lead to defaults and a cascading series of losses.

- Confidence effects: A sharp decline in the value of Bitcoin could also undermine confidence in cryptocurrencies more broadly, potentially leading to a decrease in adoption and investment.

- International spillovers: If the selloff in Bitcoin is large enough, it could potentially spill over into other financial markets and lead to broader economic impacts, particularly in countries with a significant exposure to Bitcoin.

In conclusion, Bitcoin is a complex and innovative technology that has the potential to revolutionize the global financial system. However, it is not without its risks and potential dangers, and investors should approach it with caution and do their research before investing. Ultimately, the future of Bitcoin and other cryptocurrencies remains uncertain, but it is clear that they are here to stay and will continue to shape the future of finance and technology in the years to come.

BLOCKCHAIN

The term “blockchain” was first used in the Bitcoin whitepaper, published in 2008 by an individual or group of individuals operating under the pseudonym “Satoshi Nakamoto.” In the paper, the term was used to describe the distributed database technology that underlies the Bitcoin network, which allows for the secure and transparent storage of transaction data.

Since the publication of the Bitcoin whitepaper, the term “blockchain” has become widely used to describe any distributed ledger technology that uses cryptographic methods to secure data and transactions. The term has also been applied to a range of applications beyond cryptocurrency, including supply chain management, digital identity verification, and more.

CBDC is not Bitcoin

CBDC stands for Central Bank Digital Currency. It is a digital form of fiat currency that is issued and backed by a central bank. CBDCs are essentially digital versions of physical cash, and they are designed to be a secure and efficient means of payment that can be used for everyday transactions.

Bitcoin and other cryptocurrencies, on the other hand, are decentralized digital currencies that are not backed by any government or central authority. Instead, they are based on blockchain technology, which is a distributed ledger that records all transactions in a secure and transparent manner.

Bitcoin and other cryptocurrencies have gained popularity in recent years as an alternative to traditional forms of currency and payment systems. They are often used for online purchases, peer-to-peer transactions, and as a speculative investment.

The key differences between CBDCs and cryptocurrencies are their issuers and their underlying technologies. CBDCs are issued and backed by central banks, while cryptocurrencies are decentralized and not backed by any government or central authority. Additionally, CBDCs are likely to be based on centralized technologies that are controlled by central banks, while cryptocurrencies are based on decentralized technologies that are controlled by a distributed network of users.

Has blockchain been overhyped

It’s fair to say that blockchain has received a great deal of attention and hype in recent years, and some experts have argued that the technology has been overhyped. While blockchain certainly has the potential to revolutionize many industries, it’s important to be realistic about its capabilities and limitations.

One of the main challenges facing blockchain technology is scalability. While blockchains are highly secure and resistant to tampering, they can also be slow and resource-intensive. This has made it difficult for blockchain to compete with more traditional technologies in certain areas, such as payment processing or high-volume data storage.

In addition, there are still many unanswered questions around the legal and regulatory framework for blockchain, particularly in areas like taxation, intellectual property, and consumer protection. These issues will need to be addressed before blockchain can achieve widespread adoption in many industries.

Investing Today

Investing today is largely achieved using computers. For example Renaissance Technologies is known for its use of sophisticated computer algorithms to analyze vast amounts of market data and identify profitable trading opportunities. The firm’s trading strategies are based on a wide range of factors, including market trends, economic indicators, and even satellite imagery.

One of Renaissance Technologies’ most successful funds is the Medallion Fund, which has consistently delivered extremely high returns to investors. The fund is only available to current and former employees of Renaissance Technologies, and it is known for its extremely high fees and exclusivity.

Renaissance Technologies’ success has made it one of the most profitable hedge funds in history, and it has attracted the attention of investors, academics, and regulators alike. However, the firm’s trading strategies and algorithms are highly proprietary and closely guarded, and little is known about how they actually work.

Some of the most common types of computer trading systems include:

- Algorithmic trading systems: These are computer programs that use mathematical algorithms to execute trades automatically based on pre-set criteria, such as market trends, volume, or price movements.

- High-frequency trading (HFT) systems: These are algorithmic trading systems that use advanced technology and high-speed data networks to execute trades at incredibly fast speeds, sometimes in microseconds.

- Quantitative trading systems: These are trading systems that use statistical models and mathematical algorithms to identify trading opportunities and manage risk.

- Machine learning and artificial intelligence trading systems: These are more advanced trading systems that use artificial intelligence and machine learning techniques to analyze large amounts of data and identify patterns that may be difficult or impossible for human traders to detect.

- Sentiment analysis trading systems: These are trading systems that use natural language processing and machine learning techniques to analyze news articles, social media posts, and other sources of data to gauge investor sentiment and predict market movements.

Overall, computer-based trading systems have become increasingly popular in recent years, as they offer a range of benefits over traditional manual trading, including speed, accuracy, and the ability to analyze vast amounts of data quickly and efficiently. However, these systems also carry risks, such as the potential for glitches, bugs, or other errors that can lead to losses.

The US DOLLAR

The US dollar has been the world’s primary reserve currency for several decades, and its status as the global reserve currency plays a significant role in the US economy. However, it’s difficult to provide an exact percentage of the US economy that is dependent on the dollar’s status as the world reserve currency, as the impacts are complex and far-reaching.

Here are a few key ways in which the dollar’s reserve currency status impacts the US economy:

- Trade: The dollar’s status as the world reserve currency facilitates international trade, as many countries and businesses around the world prefer to use dollars to conduct transactions. This helps to support US exports and supports economic growth.

- Investment: The dollar’s reserve currency status also attracts significant foreign investment into the US economy, as many foreign investors prefer to hold their assets in dollars due to the currency’s stability and liquidity. This investment helps to fuel economic growth and job creation in the US.

- Monetary policy: The dollar’s status as the world reserve currency gives the US government and Federal Reserve significant influence over global monetary policy. This influence can impact a range of economic factors, including interest rates, inflation, and currency exchange rates.

The US economy is dependent on the foreign exchange market (forex) because international trade and investment are a major part of the economy. The forex market allows for the exchange of currencies between countries, which is necessary for international trade and investment. When a US company exports goods or services to another country, it will typically receive payment in the currency of the importing country. The US company may then exchange the foreign currency for US dollars in the forex market.

Similarly, when a US company imports goods or services from another country, it will typically pay for those goods or services in the currency of the exporting country, which may need to be exchanged for US dollars in the forex market. The forex market also allows for the exchange of currencies for other purposes, such as international investment and speculation. Overall, the forex market plays an important role in facilitating international trade and investment, which are critical components of the US economy.

The US is like a world bank

The US economy, and more specifically the US financial system, plays an important role in facilitating international trade and investment. The US dollar is the world’s most widely used currency for international transactions, and the US financial system is among the most advanced and sophisticated in the world. This has made the US a major player in the global financial system, and in some ways, it can be thought of as a “bank” that provides financial services to other countries and facilitates international transactions. However, it’s important to note that the US economy is much more complex than a simple bank, and its role in the global financial system is constantly evolving and changing.

https://www.jpmorgan.com/insights/research/currency-volatility-dollar-strength

The US dollar’s status as the world’s most widely used currency and the US financial system’s prominent role in the global financial system have been built up over time through a combination of historical, political, and economic factors.

One of the key factors was the Bretton Woods Agreement, which was signed in 1944 and established the US dollar as the world’s reserve currency. Under this agreement, other countries agreed to fix their exchange rates to the US dollar, and the US agreed to convert dollars into gold at a fixed exchange rate of $35 per ounce. This made the US dollar the dominant currency for international transactions, and it allowed the US to accumulate vast amounts of gold and other assets.

Another factor was the growth of the US economy and financial system after World War II. The US became the world’s largest economy and the center of global finance, with Wall Street and other financial institutions becoming key players in the global financial system.

The US also played a key role in establishing the international institutions that govern the global financial system, such as the International Monetary Fund (IMF) and the World Bank. These institutions helped to establish the US dollar as the world’s reserve currency and gave the US a prominent role in shaping global financial policies.

Overall, the US dollar’s status as the world’s reserve currency and the US financial system’s prominent role in the global financial system have been built up over decades through a combination of historical, political, and economic factors.

There were several reasons why other countries agreed to the Bretton Woods Agreement and the use of the US dollar as the world’s reserve currency.

Firstly, the US was the world’s largest economy and had the largest gold reserves at the time, so it made sense for other countries to use the US dollar as a reliable and stable currency for international transactions.

Secondly, the Bretton Woods Agreement provided a framework for stability and predictability in international trade and finance. Countries agreed to fixed exchange rates and the US committed to maintaining the value of the US dollar by pegging it to gold.

Thirdly, the US played a leading role in establishing the international institutions that governed the global financial system, such as the International Monetary Fund (IMF) and the World Bank. These institutions helped to promote global economic growth and provided financial assistance to developing countries.

Finally, many countries were still recovering from the devastation of World War II and were in need of financial assistance and investment. The US provided this assistance through the Marshall Plan, which helped to rebuild Western Europe and promote economic stability and growth.

Not all countries were necessarily happy with the Bretton Woods system and the use of the US dollar as the world’s reserve currency. However, most countries ultimately agreed to participate in the system as it provided stability and predictability in international trade and finance.

One notable example of a country that did not fully participate in the Bretton Woods system was France. In the 1960s, France began to build up large dollar reserves and became concerned about the US’s ability to maintain the value of the dollar. In 1965, France withdrew its gold reserves from the US and converted them into dollars, which put pressure on the US to maintain the value of the dollar. In 1971, the US government announced that it would no longer exchange dollars for gold, effectively ending the Bretton Woods system.

Other countries also expressed concerns about the US’s ability to maintain the value of the dollar, and there were criticisms of the Bretton Woods system from some developing countries that felt it did not do enough to promote their economic development. However, despite these criticisms, most countries ultimately agreed to participate in the system as it provided stability and predictability in international trade and finance.

What was so stable about the US compared to other countries after WW2?

After World War II, the US emerged as the world’s dominant economic and military power. The US had the largest and most productive economy in the world, with a strong industrial base, abundant natural resources, and a well-educated workforce. Additionally, the US had largely been spared the physical devastation of the war, which had ravaged many other countries.

This relative stability and strength of the US economy made the US dollar an attractive currency for other countries to hold as a reserve. The US also played a leading role in the reconstruction of Europe and Japan after the war, which further enhanced its global standing and influence.

In addition, the US government took steps to establish and maintain a stable international monetary system. The Bretton Woods system, which was established in 1944, provided a framework for fixed exchange rates between currencies and allowed for the free convertibility of currencies into dollars. This system provided a level of stability and predictability in international trade and finance that was attractive to many countries.

Why was our economy so strong?

The US had several factors that contributed to its strong economy after World War II:

- Strong Industrial Base: The US had a highly productive industrial sector, which included the production of steel, automobiles, and other goods. This enabled the country to export goods to other countries and generate revenue.

- Technological Innovation: The US was a leader in technological innovation and research, which gave the country a competitive edge in many industries. For example, the development of computer technology in the 1960s and 1970s gave rise to the information age and created many new industries.

- Natural Resources: The US had abundant natural resources, including oil, coal, and iron ore. This enabled the country to produce energy and raw materials domestically, reducing reliance on imports.

- Stable Political System: The US had a stable political system with a strong rule of law, which helped to create a favorable environment for investment and economic growth.

- Human Capital: The US had a highly educated and skilled workforce, which was crucial in the development of high-tech industries and the knowledge economy.

Overall, these factors contributed to the US’s strong economic performance after World War II and helped to establish the US as the world’s dominant economic power.

Outsourcing of production is one factor that has contributed to the decline of certain sectors of the US economy, such as manufacturing. However, it’s worth noting that the US economy is still one of the largest and most diverse in the world, with strengths in areas such as technology, finance, and healthcare. Additionally, outsourcing can also have benefits, such as lower prices for consumers and increased efficiency for businesses. The overall impact of outsourcing on the US economy is a complex and controversial topic, and opinions vary widely on its effects.

Is America’s economy mostly based on services

Yes, the US economy is largely based on services. In fact, the service sector makes up the largest share of the US economy, accounting for around 80% of the country’s gross domestic product (GDP). Some of the largest service industries in the US include healthcare, finance, retail, professional and business services, and entertainment. While manufacturing and other industries still play important roles in the US economy, the service sector has become increasingly dominant in recent decades.

Has this contributed to a worsening income inequality?

Yes, the shift towards a service-based economy in the US has contributed to a worsening of income inequality. This is because service jobs, particularly in lower-skilled service industries such as retail and hospitality, tend to pay lower wages than jobs in manufacturing and other industries. This has led to a concentration of wealth and income among a smaller segment of the population, as well as a decline in the middle class. Additionally, the increasing importance of education and specialized skills in the service sector has further widened the gap between those with higher education and those without.

What is the outlook?

The outlook for income inequality in the US and UK is uncertain. While some economists and policymakers argue that economic growth and technological advancements can help to address inequality, others argue that these factors may actually exacerbate the problem. The COVID-19 pandemic has also had a significant impact on income inequality, with low-wage workers and minority groups disproportionately affected by job losses and reduced incomes.

https://www.cnn.com/2023/02/14/economy/uk-strikes-wages-inflation/index.html

There are various proposed solutions to address income inequality, such as raising the minimum wage, strengthening labor protections, increasing access to education and training programs, and implementing progressive taxation policies. However, there is ongoing debate and political polarization around these issues, and it remains to be seen what policies will ultimately be enacted and their effectiveness in addressing income inequalities.

it is kind of serendipitous that you are covering this topic this week,. I am currently reading (and trying to reread) a book on finance this week, that covers many of these same topics) (Bretton Woods agreement, questions surrounding the origins of Bitcoin, CBDC, the historical role of the US dollar as the worlds reserve currency, etc. etc. I am thankful my security is in Christ alone….”if riches increase, set not your heart upon them…” You are definitely a thinker! Keep writing..some of this is bound to sink into my brain. 🙂

That’s cool! Which book ? I did some more research on CBDCs tonight. Based on what I read, the banks have a lot to lose if it is implemented , so they are probably doing all they can to put out negative information. There’s still a lot of things that will have to happen before it could be rolled out and I don’t think cash will go away completely, at least not initially. AI might be a bigger threat to society in the short term . Not being able to tell what’s real is a very big problem. But yes, we can trust Him. 🙏

Look for an e-mail from me in answer to your question about the book 😉

Interesting article! Kind of long for a blog, but very informative and well presented! You should be teaching university students!

❤️&🙏, c.a.