“Tax the rich!” is a common cry amongst politicians seeking votes. Rarely do they mention the impact that raising taxes has on the economy, wages, and global trade.

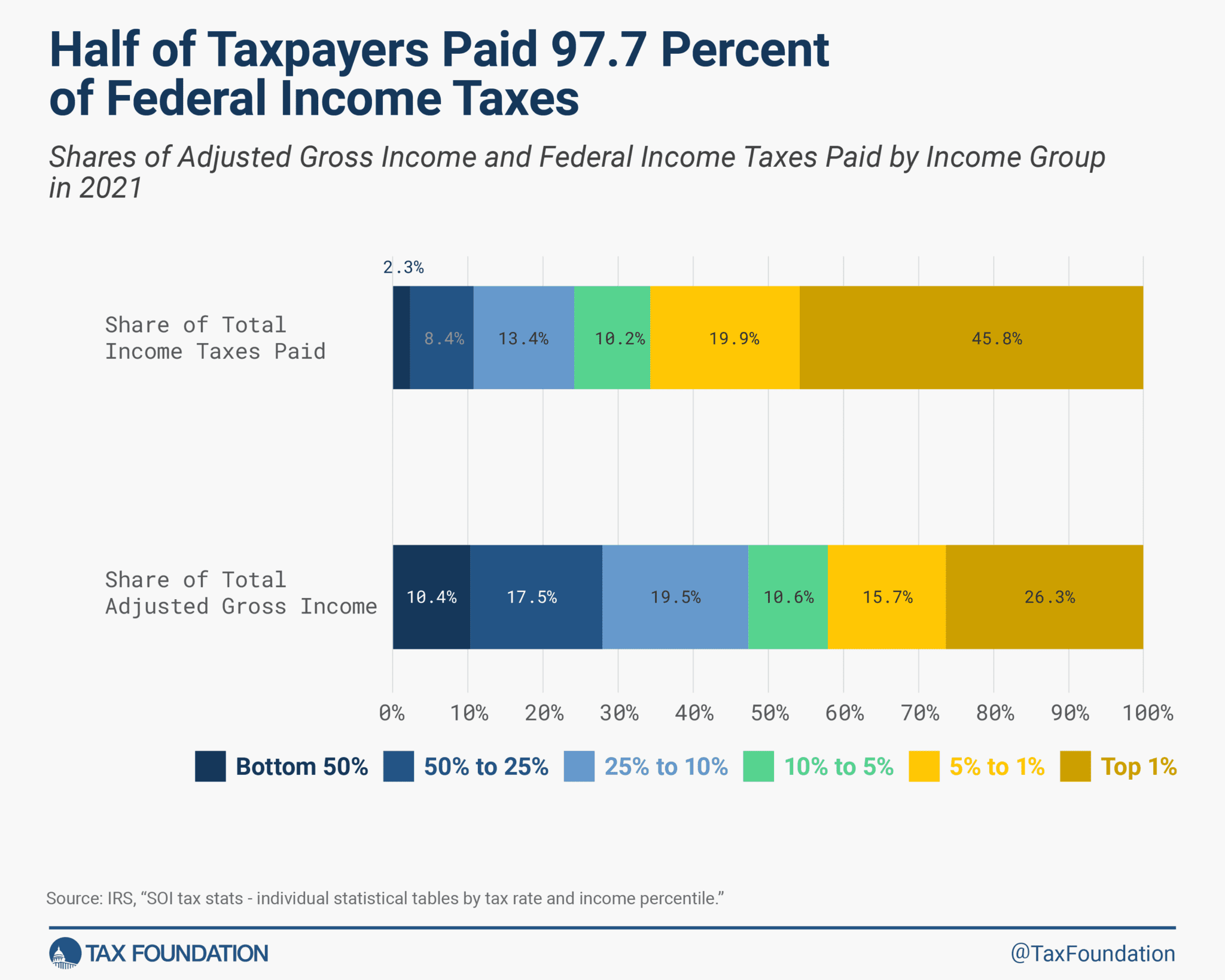

In the ongoing debate about tax fairness, a common narrative suggests that “the wealthy don’t pay their fair share” in taxes. However, a closer look at the tax system reveals that the rich actually bear a significant tax burden across various forms of taxation. From income and investment taxes to sales taxes on luxury items, the wealthy contribute more in absolute terms—and often in relative terms—than the middle class. This media talking point is a distraction from the true issue: wasteful federal spending.

1. Progressive Income Taxes: The Wealthy Pay Higher Rates

The U.S. tax system is designed to be progressive, meaning that as income increases, the percentage of income paid in taxes also rises. For example, the top marginal tax rate in 2023 is 37%, which applies to income over $578,125 for single filers and $693,750 for married couples filing jointly. In contrast, middle-class taxpayers might fall into the 12% or 22% tax brackets, significantly lower than the rates faced by high earners.

Moreover, the wealthy often have a substantial portion of their income subject to the additional 3.8% Medicare tax, which applies to earnings over $200,000 for single filers and $250,000 for married couples. This means that high-income individuals can be paying a top marginal tax rate of over 40% when state taxes are included.

2. Net Investment Income Tax: A Targeted Tax on the Wealthy

On top of income taxes, high earners are subject to the Net Investment Income Tax (NIIT), a 3.8% tax on investment income for individuals with a Modified Adjusted Gross Income (MAGI) above $200,000 (single) or $250,000 (married filing jointly). This tax applies to income from interest, dividends, capital gains, rental income, and other forms of passive income.

For example, if a wealthy individual has $100,000 in capital gains, and their MAGI exceeds the threshold, they would pay 3.8% of that $100,000 in NIIT—on top of any capital gains tax owed. This is an additional tax layer that middle-class earners, who typically don’t surpass these income thresholds, often avoid.

3. Capital Gains Taxes: A Lower Rate, But Still Significant

Capital gains—profits from the sale of investments held for more than a year—are taxed at rates of 0%, 15%, or 20%, depending on the taxpayer’s income. Although these rates are lower than ordinary income tax rates, they still represent a significant tax burden for the wealthy, who derive much of their income from investments.

In addition to the capital gains tax, high-income earners face the NIIT on their investment income, further increasing their effective tax rate on these earnings.

4. Sales and Luxury Taxes: The Hidden Tax Burden

While income and investment taxes are often discussed, the impact of sales taxes on the wealthy is less frequently mentioned. Wealthy individuals tend to spend more, particularly on high-ticket items like luxury cars, yachts, jewelry, and high-end real estate. These purchases not only incur standard sales taxes but can also be subject to additional luxury taxes.

For instance, purchasing a luxury vehicle might not only involve a higher sales tax due to the vehicle’s cost but also specific taxes designed for high-value items. Similarly, property taxes on high-value real estate properties can be substantial, especially in states with high property tax rates. These taxes add up quickly, representing a significant ongoing tax burden for the wealthy.

5. Property Taxes: A Heavy Hit for High-Value Homes

Property taxes are another area where the wealthy contribute more. High-value homes are taxed at the same rates as more modest properties, but the absolute dollar amount is far greater. For example, a 1% property tax on a $2 million home results in a $20,000 tax bill, far more than what a middle-class homeowner would pay on a $200,000 home.

In some states, property tax rates are even higher, and additional taxes might apply to particularly high-value properties. These taxes are recurring, creating an ongoing financial obligation for the wealthy that significantly adds to their overall tax burden.

Conclusion: The Rich Already Pay Their Share—and Then Some

The idea that the wealthy don’t pay enough in taxes overlooks the multiple layers of taxation they face. From progressive income taxes and the NIIT to sales taxes on luxury goods and hefty property taxes, the rich contribute a substantial amount to public coffers. In many cases, their effective tax rates are higher than those of the middle class, especially when all forms of taxation are considered.

This isn’t to say that discussions about tax policy and fairness aren’t important—they certainly are. But it’s crucial to ground these discussions in the reality that the wealthy already face a complex and significant tax burden, one that is often far greater, both in percentage and absolute terms, than what is borne by the middle class.

The real issue is a bloated federal budget with far too many people getting a piece of the pie before the taxpayers get their money back in federal services, healthcare, and social welfare programs.

What about corporate taxes? Are corporations paying their ‘fair share’? And what happens when corporate taxes are raised?

The relationship between corporate tax rates and wages is a complex and often debated topic in economics. Historically and across different countries, there have been various studies and perspectives on how changes in corporate tax rates impact wages. Here’s a summary of the key findings and considerations:

1. Theoretical Framework: Corporate Taxes and Wages

- Incidence of Corporate Taxes: In economic theory, the incidence of corporate taxes—who ultimately bears the burden—can fall on various groups, including shareholders, workers, and consumers.

- Shareholders might bear the burden through reduced dividends or capital gains.

- Workers could see the burden through lower wages or reduced employment opportunities if companies cut costs in response to higher taxes.

- Consumers might face higher prices if companies pass on the tax costs.

- Capital Mobility: In a globalized economy, where capital is more mobile than labor, higher corporate taxes might lead companies to invest less domestically or move operations to lower-tax jurisdictions. This can theoretically reduce domestic capital investment, which could, in turn, lower productivity and wages for workers.

2. Empirical Studies: Impact of Corporate Taxes on Wages

A simple Google search you will provide both positive and negative opinions on how corporate taxes effect wages, but if you look at long-term studies, the evidence shows that lower corporate taxes benefit workers.

While the paper provides useful insights into the short-run effects of corporate tax cuts, it does not examine the long-run effects—and most research shows that in the long run, corporate tax cuts can benefit all workers, not just workers at the top of the income distribution. https://taxfoundation.org/blog/corporate-tax-cuts-worker-wages/

- Mixed Results: Empirical studies on the impact of corporate taxes on wages have produced mixed results. The outcomes often depend on the specifics of the tax system, the mobility of capital, and the overall economic environment.

- United States:

- Some studies in the U.S. suggest that a portion of the corporate tax burden is passed on to workers in the form of lower wages. For instance, a study by the Congressional Budget Office (CBO) estimated that workers bear about 25% of the corporate tax burden.

- Another study by economists like Kevin Hassett and Aparna Mathur found that a 1% increase in corporate tax rates could lead to a 0.5% decrease in real wages.

- Corporate Tax Reform and Wages: Theory and Evidence

- The Efficiency-Equity Tradeoff of the Corporate Income Tax: Evidence from the Tax Cuts and Jobs Act

- European Union:

- Research by the European Commission found evidence that higher corporate taxes are associated with lower wages, particularly in countries with open economies where capital can easily move across borders.

- A study by Mihir A. Desai, Fritz Foley, and James Hines found that workers bear a significant portion of the corporate tax burden in the form of lower wages, particularly in smaller, open economies.

- Developing Countries:

- In developing countries, where capital is less mobile, the impact of corporate taxes on wages may be less direct. However, higher corporate taxes could still lead to reduced investment and slower economic growth, which could eventually impact wage levels.

3. International Comparisons

- Nordic Countries: Countries like Sweden and Denmark, which have relatively high corporate tax rates (though often coupled with high levels of public investment in education, infrastructure, and social services), have not seen a straightforward reduction in wages. The impact of corporate taxes in these countries is mitigated by the broader social contract and public services that support workers.

- Ireland: Ireland’s low corporate tax rates have attracted significant foreign direct investment (FDI), contributing to high wage growth, especially in sectors like technology and pharmaceuticals. This has been cited as an example of how lower corporate taxes can attract investment and boost wages.

- Germany: Germany, with its strong manufacturing base and relatively high corporate taxes, has maintained high wage levels. The German model relies on a mix of strong labor unions, vocational training, and industrial policies that have supported wage growth despite higher taxes.

4. Policy Considerations

- Elasticity of Capital: The impact of corporate taxes on wages is influenced by the elasticity of capital—how easily capital can move in response to tax changes. In highly globalized economies, where capital is more mobile, higher corporate taxes might lead to capital flight and downward pressure on wages.

- Complementary Policies: The effects of corporate taxes on wages can also be influenced by other policies, such as labor market regulations, minimum wage laws, and social safety nets, which can help protect workers from potential negative impacts.

- Corporate Tax Cuts: The argument for corporate tax cuts often hinges on the idea that reducing taxes will lead to increased investment, higher productivity, and, consequently, higher wages. However, the extent to which this happens in practice can vary widely depending on the broader economic context.

Conclusion

Historically and across different countries, the impact of corporate tax rates on wages has varied depending on numerous factors, including the mobility of capital, the structure of the economy, and the presence of complementary policies. While there is evidence to suggest that higher corporate taxes can lead to lower wages, particularly in open economies, the relationship is not always straightforward. In some cases, the impact may be mitigated by public investment and social policies, while in others, lower corporate taxes have been associated with wage growth, particularly when they attract foreign investment.